Creating a budget for savings is one of the toughest financial habits. It gives you control over your money, helps you avoid unnecessary debt, and ensures you’re setting aside funds for both short-term needs and long-term goals.

The sad reality is that many individuals work hard, make a decent income, and still struggle to save money.

They checked their bank accounts at the end of the month and wondered where they had spent all the money they earned.

After all, why does saving become an afterthought? And why do people save only when there is money left at the end of the month?

With the right budget, saving can become part of your financial routine, not just a hope.

What You’ll Learn

ToggleWhy Budgeting for Savings Matters

Budgeting for savings is a crucial step toward gaining control over your finances. Savings are sometimes entirely ignored when there is no strategy in place.

After spending, many people plan to save what’s left over, but in reality, there’s barely nothing is left. Here are two reasons that better explain why.

1. Emergency Ready

Before we dig down, consider this scenario, Yeol spends all his earnings. One day, he is fired from his job, and does not have enough money to cover his expenses for the month. Instead, if he has an emergency fund, then it is not difficult.

This is a fact, not fiction. Saving money can help you create an emergency fund that will protect you when you need it most.

2. Achieving Goals

Everyone dreams of a better life, but there is not enough money to make it come true. The question is whether budgeting helps to achieve that dream.

When you include savings in your budget, over time you will easily ace goals like travel, buying a home or a car, and retiring comfortably.

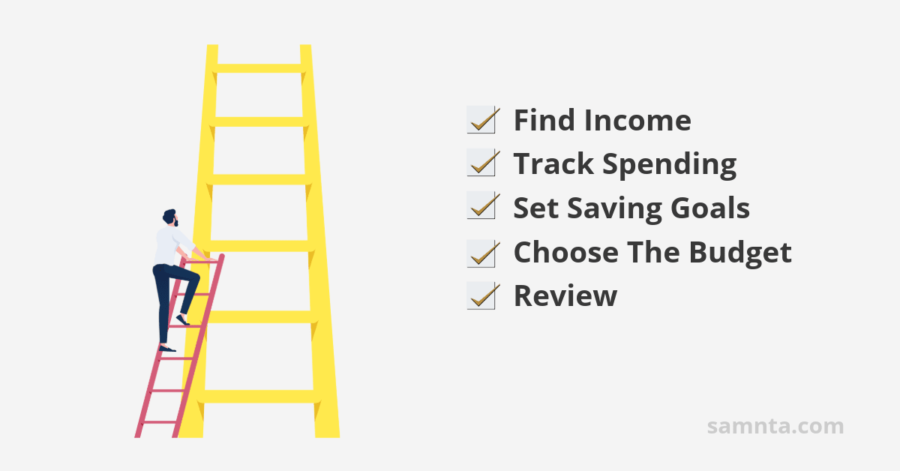

Steps to Budget for Savings

Step 1: Know Your Income

Before creating an effective budget for savings, you need a clear picture of how much money you earn.

Finding out your total income is very simple. Write down all income sources, including salary, freelancing, side gigs, rental income, government benefits, or even dividends.

Use net income, which is the amount you get in bank accounts after paying taxes or deductions. Using gross income create a unrealistic budget that not work.

Let’s say your total income is $10,000 per month (this is your gross income), after paying taxes and any debts, it finally becomes $8,200 (this is your net income).

Just think, when you make a budget based on $10,000, where will you manage $1,800 from.

Step 2: Track Your Spending

Once you know how much you earn, it’s time to understand where you spend. Because saving without knowing your expenses is not easy.

First, look at bank statements, receipts and transactions to get a rough idea of expenses. Then, make a list of all expenses, including rent, food, groceries, subscriptions, internet, bills, eating out, shopping, clothing, transportation or gifts.

You included non-essential costs in this list. These are the costs you can avoid or put off before incurring. You may plug this gap to save money.

Step 3: Set Clear Savings Goals

It is time to decide what you want to save for, as you are now aware of your income and spending patterns.

Without a clear savings goal, your budget will be aimless. Give your budget a purpose, like creating an emergency fund, paying off debt, buying a new home, buying a car, or planning a vacation.

If your savings goals are more than one, then categorise them. Which makes them easier to manage.

Step 4: Choose a Budget Method

Choosing a budgeting method isn’t easy. However, here are three well-liked methods that focus on saving money. Each method helps you build a budget for savings in a way that fits your lifestyle:

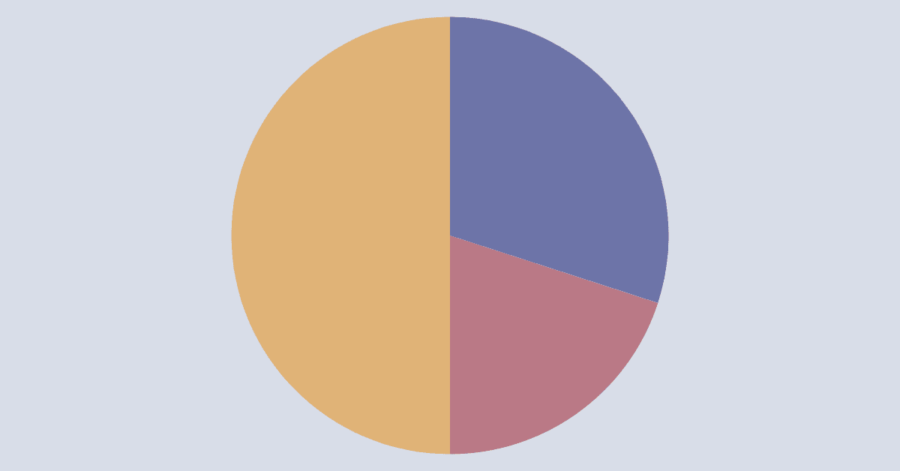

1. 50/30/20 Rule

This method allows you to save 20%. It’s easy to use and is perfect for beginners looking for a balanced approach.

2. Pay Yourself First

In this method, you prioritise saving before spending. This is great for people whose first priority is savings.

3. Custom Budget

If you have specific savings goals or your income is irregular, a custom budget lets you spend and save based on your unique situation.

Step 5: Review Regularly

Budgeting is not something you make once and think it will work fine.

Let’s imagine a situation, you eat regularly, and obviously you decide regularly what you want to eat.

Now let’s understand the same situation through budgeting. When you review the budget regularly and adjust it if needed, it works fine.

Many people complain that their budget is not working. Reason is simple. So the question is why should we review the budget regularly?

You know that life is changing rapidly. For obvious reasons, income fluctuates, expenses increase, and priorities shift.

Regular reviews help you keep up with these changes, rather than getting left behind.

Conclusion

Creating a budget for savings is one of the wisest steps you can take. It gives your money a purpose, provides long-term security and helps you be prepared for life’s surprises.

By knowing your income, tracking expenses, setting clear goals, choosing the right method and reviewing regularly, you can turn saving from a challenge to a habit.

Remember, start small, maintain consistency and if the budget isn’t working at the beginning of the week, wait for the month and find out the reason, then change the method.

FAQs

What is a Budget for Savings?

A savings budget is a plan that allocates a percentage of your monthly income to achieve savings goals.

How much should I Save each month?

Although there is no fixed amount but save at least 20% of your income, remember even a small amount can grow over time.

Why is Budgeting Important for Saving Money?

Budgeting for savings helps you prepare for emergencies and reach your financial goals.