Making a budget is one of the most important tasks that can lead to a stable financial future. Surprisingly, creating a budget is not complicated. Learning how to budget money effectively can help whether you’re trying to save more money, pay off debt, or even find your spending.

A budget might be weekly, monthly, or annual. It gives a clear purpose to every penny.

What You’ll Learn

ToggleBudget Meaning

A budget is a plan that guides how your money flows. Generally, how you earn, spend, save, and handle your money. In short, it is a blueprint for your finances.

The word “budget” is not original, it actually comes from the Old French word “bougette”, which means “small bag.”

In ancient times, a small leather pouch called a bougette was used to carry coins.

Over time, the word – especially in British times – has become more used in revenue terms.

Where Are Budgets Used?

Budget isn’t just only use for big corporations or financial experts, it’s useful in everyday life. Whether you are a couple, a student, or a business owner. Here are common examples:

1. Households

Families and individuals use a budget to monitor income, find spending, and future goals like buying a house, a car, a vacation, or a retirement plan.

A household budget mostly includes rent, utilities, mortgage, groceries, and savings categories.

2. Students

Budgeting for students might seem to be difficult with no income source, a part-time work income, scholarships, or student loans.

A student budget keeps track of expenditures such as tuition, books, food, and social activities, ensuring that enough money is left over to pay for necessities.

3. Small Businesses

Small business owners (whether they are entrepreneurs, freelancers, or influencers) use budgets to estimate their revenue.

A business budget helps to monitor losses, ensuring profit.

Steps to Budget Money

It doesn’t matter how much you earn or how rich you are, the budget depends on income and where you spend. It’s the same whether you live in any corner of the world. Here’s are step-by-step budgeting guide:

Step 1: Know Total Monthly Income

Many of us have no idea how much we make; instead, we just check how much is left and spend like a sloth.

How to find the total monthly income is very easy. Check bank accounts – whether it is a salary, wages, freelance, side gig, pensions, or business income – and get an idea.

If you have irregular income, then take an average of the last 3 to 5 months.

Step 2: List All of the Monthly Expenses

Write down the spending amount – easily find on the bank statements or mobile money transactions – and divide your expenses into two categories.

Fixed expenses include rent/mortgage, utilities, internet, tuition, transportation, and insurance.

Variable expenses include groceries, eating out, clothing, entertainment, data/airtime, and personal care. Don’t assume a lump sum amount.

Step 3: Categorise Spending

Breaking down your expenses into categories helps you cover essential expenses first.

Common spending categories are rent, food, transportation, utilities, debt repayment, savings, and other expenses.

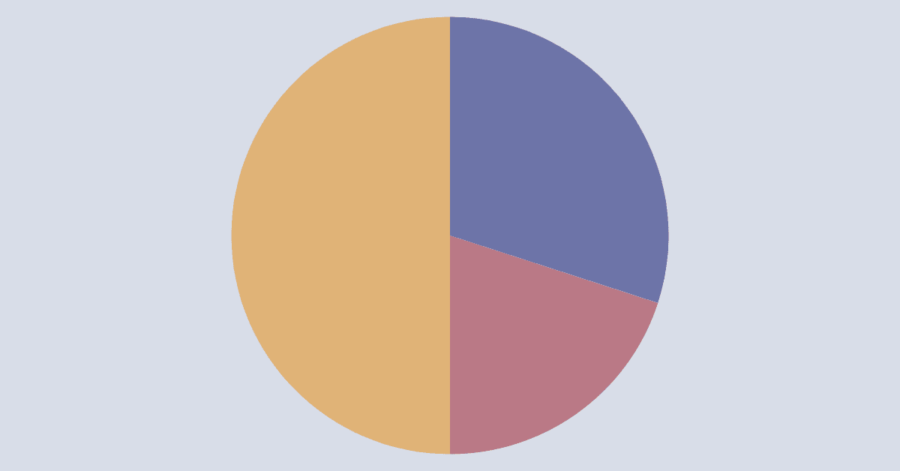

Try the well-known 50/30/20 budget plan if you’re having trouble categorising and prioritising. Whereas 50% of your income is spent on needs, 30% on wants, and 20% on savings or debt reduction.

Step 4: Find Out What is Left

It is very easy to find out how much money is left. Do a simple maths work, subtract expenses from income, and get what’s left.

Left a lot then allocate it to savings, emergency funds, debt payments, or retirement accounts.

If, Nothing is left then cut expenses from eating out, subscriptions, shopping, or increase your income (that’s damn good).

Step 5: Choose a Budgeting Method

Different people prefer different budgeting methods. There are no specific criteria for picking a suggested budget.

Try all methods – if you are confused to pick the right one – and consider one of them that fits your lifestyle. Here are common methods, choose what fits:

1. Spreadsheet

One of the most effective ways to make and manage a budget. These are free and safer for privacy reasons.

You can create a budget using Google Spreadsheets or Excel. There are free or paid budget templates available.

2. Notebook

If books are your favourite, then a Notebook for a budget is the best option. It is simple and manual with More safer for privacy reasons.

You can buy a budget notebook, including a monthly calendar, from a bookstore or online.

In starting seems more difficult to make a budget, track expenses. But over time, it has become more friendly.

3. Budgeting Apps

Mint or YNAB are the best fit if you want a tension-free and easy interface for budgeting.

But don’t forget budgeting apps’ privacy, some budgeting apps share your data with third-party loans and credit card companies.

4. Envelope System

Most loved, also known as an old school method or cash stuffing. In this budgeting method, use cash envelopes for each category, whether it is for expenses, savings, or future plans.

5. Mobile Banking Tools

Many banks now offer budgeting features with more safety due to financial fraud (scams). You may be too frustrated to use banking apps because more layered security. But the features are too damn good.

Step 6: Track and Review

You can set a reminder to check your budget weekly or monthly, but sometimes it is too disruptive. After tracking, I mean set a reminder, review the budget, and adjust as needed.

Ask yourself for a better review. Are you overspending in certain areas, or can you increase your savings?

Remember, make a budget and forget it, very common. Make it a daily habit, not a one-time monthly or yearly task.

Common Budgeting Mistakes to Avoid

Budgeting is a skill that requires practice. However, being aware of the common mistakes can help you avoid unnecessary stress. Here are some budgeting mistakes and how to avoid them.

1. Not Tracking Spending

Your budget might be based more on hope than reality. This often leads to confusion about where the money went.

Rather than analysing expenses from the past 2–3 months, categorise your spending.

2. Underestimating Expenses

People often forget occasional costs like annual subscriptions, car repairs, or gifts.

It’s easy to focus on monthly bills and miss those unexpected expenses.

Rather than creating a sinking fund for those irregular costs, set up small monthly amounts like a small emergency fund for unforeseen expenses, so they don’t disrupt your budget when they hit.

3. Relying Too Much on Credit

Using credit cards to cover expenses can quickly lead to debt. This process works like a loop, as you borrow money to pay off other expenses. It’s time to find additional income sources.

4. Comparing Your Budget

It’s easy to look at someone else’s budget. But comparison leads to overspending. So, focus on your goals. Your budget should reflect your life, not someone else’s.

5. Not Updating Your Budget

If you set your budget once and never update it, it will eventually stop working.

This is when people start to feel that budgeting doesn’t work for them. Update your budget regularly or weekly, depending on your efforts.

Conclusion

Making a budget doesn’t have to be complicated. It’s simply a plan for your money. On the other hand, monitor and track your income, expenses, and savings.

The budget should give you complete clarity, control, and confidence.

Whether you’re trying to save more, spend smarter, or plan for the future. Start with a simple budgeting method that suits your lifestyle.

FAQs

What is the easiest way to create a budget?

Start by listing your monthly income and expenses. Then, separate needs from wants and set spending limits for each category.

How do I create a monthly budget for beginners?

Use a simple method like the 50/30/20 rule that has been proven to work for beginners.

What are the steps to creating a personal budget?

The basic steps to a personal budget include first, tracking your income, then listing all expenses, categorizing expenses as well, then setting goals, and finally adjusting as needed.

Why is creating a budget important?

Budgeting helps you control spending, reduce stress, increase savings, and reach financial goals.

How often should I review my budget?

Review your budget daily to keep track of it, and if you can’t, review it at least once a month.