Pay yourself first is a simple concept that conveys how you prioritize money. Many people spend their paycheck on bills, groceries, and other expenses, leaving nothing left to save at the end of the month.

According to a financial analysis, half the world’s population does not have enough savings for even three months of expenses.

With the pay yourself first budgeting method, you save money first, then spend on anything else.

What You’ll Learn

TogglePay Yourself First budgeting

Definition: Pay Yourself First is a budgeting method where your first priority is to save money instead of spending anywhere else. The concept is based on the belief that savings should come first, not last.

Origin of the Concept: The idea of Pay Yourself First has been around for decades and popularized by personal finance advisors David Bach and Robert Kiyosaki.

Real Life Example: Let’s take Sarah, a graphic designer who earns $4,000 a month after taxes.

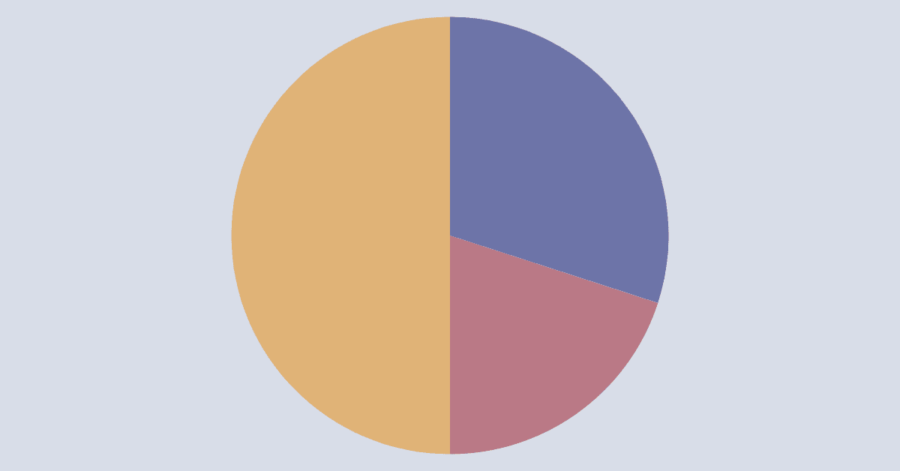

Instead of waiting until the end of the month to save, Sarah decides to “pay herself first” by setting aside $800 (20%) from every paycheck as soon as she gets paid.

She puts $400 into a high-interest savings account, $200 into her retirement fund, and $200 into an emergency fund.

This leaves her with $3,200 to cover rent, bills, groceries, and other expenses. Using the Pay Yourself First method, Sarah creates steady savings.

How to Start Paying Yourself First

The Pay Yourself First budgeting method helps you build savings by giving it top priority. Here’s a step-by-step guide to get started:

Step 1. Find Out Earnings

You must figure out your actual income before deciding how much to save. Calculate your net income after taxes, including all sources, whether it is a salary, side gigs, or a bonus.

Net income helps to figure out how much money to save and spend.

Step 2. Set Savings Goals

This budget especially focuses on savings. So, find out your saving goals and decide where you’re saving, like in a savings account, retirement planning account, or in the form of an emergency savings fund.

Major savings goals are to build an emergency fund, plan for retirement, vacation, house, or pay off debt fast. These savings goals help you to stay focused and achieve faster.

Step 3. Decide How Much to Save

How much to save is different for everyone, but most recommend 10% to 20% of net income. If you have higher expenses, start small, like 5%, then gradually increase it.

Step 4. Automate Your Savings

If you want to pay yourself first, automation is necessary.

When your income is credited to your account, automate a transfer fix amount to your savings account.

Some accounts allow scheduling transfers, because we frequently forget to save money in our hectic lives. Automation helps you stay consistent.

Step 5. Budget What’s Left

Now that you’ve paid yourself first, I mean, how much do you save for yourself? Now let’s talk about the balance, so use the remaining income to cover your monthly expenses.

These expenses are fixed and variable. Fixed expenses are rent, utilities, food, and groceries.

Additionally, transportation, entertainment, food, and the internet are variable costs.

If you struggle to create a budget, you simply use spreadsheets and adjust accordingly, which will help to set up your first budget.

Step 6: Adjust Regularly

Making a budget is not enough; you also need to make updates to it on a daily basis.

Most budgets fail due to a lack of adjustments and regular review. For motivation, try setting small milestones that will help you stay on track.

Best Accounts for Pay Yourself First

When you follow the pay yourself first budget, you need the right type of accounts. Here are the best types of accounts to consider:

1. Traditional savings account

Best for: All types of savings goals

2. High-Yield Savings Account

Best for: Emergency funds, short-term savings

3. Retirement Accounts (e.g., IRA, Roth IRA, 401(k))

Best for: Long-term retirement planning

4. Investment Accounts

Best for: Long-term wealth building

5. Health Savings Account

Best for: Managing medical emergencies

Pay Yourself First Budgeting Mistakes

It is very common to make mistakes while budgeting pay yourself first, but ignoring them leads to a delay in your savings goals. Here are some common mistakes to avoid:

1. Not adjusting Savings

This mistake happens often. When you earn from a certain job as well as from other sources, the income is not the same.

Read Also: How To Budget With Irregular Income

Or it may be that your income is the same, but this month you spent more on unexpected expenses. Therefore, you need to adjust savings accordingly to net income.

2. Underestimating Monthly expenses

When you first start paying yourself, you set high savings goals, and over time, you realize that your expenses are much more than that. And you often make this mistake.

So, before you dig deeper into your budget, make sure you know how much you spend and how much you save.

3. Not Automating The Process

Automation helps in transferring money to savings accounts when money is credited in the account. This reduces the risk of not saving and helps in managing the budget. The problem occurs when we forget to automate and do the transfer manually. If you are a beginner, start with less.

Conclusion

Pay yourself first is very simple for those who have savings goals. These savings goals can be for anything, whether it is for the future, retirement, an emergency, or buying a house.

Creating a budget is easy, but not adjusting it makes it difficult to manage. This is ideal for savings goals.

Share your thoughts in the comments. Your story might inspire someone else!